The Undisputed Champion of Luxury

We first wrote this piece in the fall of 2025. We’re sharing it now in its original form because the underlying argument has held up — and in several places, has been reinforced — by subsequent events. In the months since, the company has announced US expansion plans, Swiss tariffs have been significantly reduced, and the setup we laid out then has only gotten more compelling. This is all despite the global macroeconomic uncertainty that has accompanied the past few months. Rather than rewrite history with the benefit of hindsight, we’d rather show our work as it stood — and let the subsequent performance speak for itself. Our conviction today is higher than when we first put pen to paper.

October 2025

At a time when cars converge into indistinguishable silhouettes and artificial intelligence threatens to erode individuality, mechanical watches remain defiantly human, They are not fashion. They are permanence, emotion, and meaning made manifest in steel and gold. - Hind Seddiqi, CEO of Dubai Watch Week

Executive Summary

Elevator Pitch: Watches of Switzerland Group (WOSG) is a dominant luxury watch retailer – effectively the listed proxy for Rolex – trading at distressed multiples despite robust fundamentals. WOSG commands ~ 50% of Rolex sales in the UK and is the largest player in the fragmented U.S. market. The business model is uniquely attractive: 100% full-price sales, multi-year waitlists, no inventory or online pricing risk, and yielding ~ 20% store-level margins. Yet the stock has collapsed ~75% from 2022 highs on fears that Rolex’s acquisition of retail peer Bucherer signals distribution disintermediation, compounded by post-COVID deflation for secondary watch prices. At ~ 9x depressed earnings, with a pristine balance sheet and ~ 20-30% historical ROIC, the market is pricing WOSG as if its franchise is impaired. Our thesis is that this mispricing is unwarranted – WOSG’s relationship with Rolex is as strong as ever, and structural growth opportunities (U.S. consolidation and Certified Pre-Owned) remain sizable. We see an asymmetric reward-risk profile with 100% + upside and limited downside, driven by misunderstood dynamics in supply, expansion runway, and resilience of demand.

Variant Perception: Consensus perceives WOSG as a structurally imperiled “middleman” and remains overly fixated on near-term headwinds – US tariffs, soft UK demand, constrained supply, and the misperception that Rolex might favor its newly acquired Bucherer network at WOSG’s expense. Our view is that Rolex’s move was defensive, not a shift to vertical integration, and that WOSG will continue to be one of Rolex’s most trusted partners. In fact, Rolex has been consolidating distribution to top retailers like WOSG, not undermining them, yet today’s price implies WOSG’s model is at serious risk of disintermediation by Rolex. We disagree. We think WOSG’s partnership with Rolex is as strong as ever, its U.S. expansion runway is underappreciated, and the recent luxury watch downturn has largely bottomed out. We expect WOSG to capture outsized growth as supply normalizes and it leverages superior scale and relationships to roll up smaller U.S. dealers. Street models underestimate the pent-up demand and pricing power in luxury watches, and the operating leverage in WOSG’s model as new volume flows through. In short, investors are missing the forest for the trees – WOSG remains firmly entrenched as a critical partner to the top brands, and its growth prospects are materially better than overly pessimistic consensus expectations.

Why the Opportunity Exists: The stock’s derating reflects transient and fixable issues. First, the 2021–22 luxury watch frenzy (skyrocketing secondary prices amidst COVID demand) inevitably cooled. This cyclical air-pocket softened sales and compressed profits, souring sentiment. Second, Rolex’s August 2023 announcement to acquire Bucherer – an iconic Swiss retailer – sent shockwaves through the market and spooked investors into assuming Rolex might “internalize” distribution or divert supply from WOSG. WOSG plunged ~ 30% on the announcement and remains a neglected orphan. These fears, while understandable, are overblown. In reality, Rolex explicitly stated it will keep Bucherer operating independently with no change to allocation processes; a message WOSG echoed in a joint release.

Industry checks confirm Rolex acted to preserve heritage (Bucherer’s founder had no succession) and to prevent an unwelcome buyer, not to run a retail chain. Multiple former Rolex insiders and experts affirm that Rolex has zero intent to restructure its century-old third-party retail model, given the fragmentation and immense cost of doing so. These overblown fears created an outsized disconnect between WOSG’s resilient fundamentals and its valuation, setting the stage for outsized gains as concerns are put to rest.

Catalyst Path: We think sentiment will inflect as WOSG delivers evidence that the feared risks are not materializing and as growth reaccelerates. Key catalysts over the next 18 months include: (1) Rolex Certified Pre-Owned (CPO) ramping – WOSG’s rollout of Rolex’s official pre-owned program (launched in 2023) is exceeding expectations and creating a new high-profit revenue stream; (2) U.S. expansion – high-profile showroom openings, new flagship boutiques, and continued accretive acquisitions showcasing momentum in one of the largest, most fragmented, and underpenetrated watch markets; (3) Clarification from Rolex – as quarters pass with no adverse allocation shifts, investor fears should abate; and (4) renegotiated tariffs on Swiss imports – providing management with the clarity needed to update investors with a refreshed long term plan. Additionally, we believe an accelerated repurchase program followed by a US listing would go a long way toward signaling management’s confidence while providing technical support to the stock. Should shares continue to trade at this severely depressed valuation, we think the company could become an acquisition target itself (channel checks suggest that if Rolex ever wanted to fully own distribution, there is only one option – acquire WOSG). In short, as WOSG continues to execute and feared scenarios fail to materialize, the value gap will close – whether through improving fundamentals, strategic action, or simply the passage of time.

Reward/Risk Snapshot: The risk-reward is compellingly skewed to the upside. There are no perfect public comps for WOSG, but related groups include European luxury brands trading at ~15–30× NTM EBITDA and U.S. specialty retailers trading as high as 15x NTM EBITDA, which we see as a more appropriate valuation level than the current 5x NTM EBITDA WOSG trades. We also looked at historical transactions of luxury watch and jewelry retailers over the past decade, which imply a WOSG per share valuation range of ~£5-24 and a median close to ~£10 per share. A brand level sum-of-the-parts whereby we apply a higher multiple for the supply-constrained brands and a lower multiple for the remainder of the business (Other Watches, Jewelry, Services) implies a WOSG per share valuation range of ~£7-14. Our base case envisions WOSG executing its growth strategy and the market assigning a still-conservative ~12-14x P/E multiple, yielding roughly ~100% upside. The bull case – in which WOSG fully delivers on its plan (or attracts a strategic suitor) – offers a potential 4-5x return. In contrast, even a bear-case outcome of prolonged downturn and margin pressure would likely cause only a modest ~25% downside, thanks to the stock’s already low valuation and solid balance sheet.

Bottom line: Given the stark disconnect between WOSG’s operational quality and its valuation, the market is offering investors an attractive asymmetric bet: limited downside (~25%) against potential returns of 100–300%+, with the company trading below the sum of its acquired parts despite consistently demonstrating its ability to extract platform value. At 5× depressed EBITDA—pricing that implies permanent impairment rather than cyclical pressure—WOSG represents either a structural value trap or a significant mispricing. We think the evidence strongly suggests the latter.

Business overview

Watches of Switzerland Group is an international multi-brand luxury watch retailer with over 220 showrooms across the UK (its home market) and the U.S. (entered in 2017). Originally founded in 1924, the company was rejuvenated in 2014 when CEO Brian Duffy (a luxury retail veteran) joined under private equity ownership (Apollo). Duffy shifted the strategy from cost-cutting to investing in customer experience and showroom expansion, which proved transformative – WOSG’s UK market share of luxury watches grew from ~ 32% in 2015 to ~ 50% by 2023. The company listed on the LSE in 2019 and has since aggressively expanded in the U.S. via acquisition and new store openings, becoming the top U.S. luxury watch retailer with ~ 10% share. Today WOSG operates a portfolio of prestige retail brands: Watches of Switzerland, Mappin & Webb, Goldsmiths (UK multi-brand chains), and Mayors, Betteridge in the U.S., alongside numerous mono-brand boutiques built on long-standing partnerships with Rolex (it became Rolex’s first authorized UK retailer in 1919), Patek Philippe, Audemars Piguet, Omega, TAG Heuer and others.

The core profit engine is new luxury watches sold through destination showrooms and branded boutiques that WOSG operates (inventory and staff are WOSG’s; the boutiques carry the brand’s identity), augmented by luxury jewelry, certified preowned (CPO), service and digital commerce. In FY25, watches represented ~ 83% of revenue, with the balance in jewelry and services. Rolex is the powerhouse representing over 50% of group sales, while the firm’s top eight luxury brands making up fully three quarters of sales, effectively placing WOSG at the epicenter of the high-end Swiss watch industry. Roberto Coin was a large acquisition WOSG completed in May 2024 (~$130m purchase price) in an accretive transaction that furthered their presence in luxury jewellery – the segment made up ~13% of FY25 sales. Geographically, revenues are evenly split between the UK and the U.S., with U.S. share roughly doubling in the past five years. The group operates two primary store formats: large multi-brand showrooms (either flagship >6,000 square foot stores offering a range of brands, often anchored by Rolex, or larger 3,000-6,000 square foot stores) have been complimented by mono-brand boutiques, as luxury brands increasingly prefer dedicated spaces to elevate the experience of a single marquee brand. It also operates a growing e-commerce platform (including a U.S. replatforming on Shopify) and a rapidly growing pre-owned segment. Notably, e-commerce remains a small share of sales but extends reach and improves conversion without diluting the category’s high touch DNA, as in-store experience is critical in this category (more below).

The WOSG Moat

Irreplaceable brand relationships and distribution rights provide WOSG with a substantial competitive moat, built upon (i) relationship capital (decades long ties; consistency of execution), (ii) destination real estate (flagships in the best locations), (iii) operational scale (assortment breadth, inter store transfers, marketing), and (iv) category authority (training, clienteling, content via Hodinkee). All of these elements combine to reinforce brand trust and allocation access as core relationships are multi-generational and cannot be replicated by new entrants. As one former Rolex employee put it, getting a Rolex AD license is “a license to print money” and “the holy grail.” No matter how much capital a would-be competitor has, they simply cannot become an authorized Rolex dealer – Rolex picks partners extremely carefully (often family businesses or trusted groups) and hasn’t added a new UK partner in decades.

We think WOSG’s century-old partnership with Rolex gives it an intangible asset as valuable as any luxury brand IP. Moreover, WOSG has substantial scale advantages which assure it remains the partner of choice: its ability to invest in ultra-premium store buildouts and omni-channel marketing far exceeds smaller rivals providing a level of service local jewelers simply cannot match. This pleases brands (Rolex rewards those who elevate the brand experience with more allocation) and attracts consumers, with stores that feature cocktail bars, and VIP lounges and events. Scale also yields operational efficiencies: centralized purchasing, a leading CRM database of high-net-worth clients, and an exclusive e-commerce platform. WOSG’s client experience program, centralized CRM, and digital upgrades tighten the loop from discovery to purchase to service to upgrade, supporting higher lifetime value as clients progress up the price spectrum.

WOSG’s multi-brand format also creates a halo effect: Rolex is the magnet drawing foot traffic, but once in-store, customers often buy other watches and jewelry; a synergy that brands appreciate because being in a Rolex-authorized store confers prestige. Finally, WOSG benefits from a well-honed client registration & waitlist system that fuels demand – their salespeople cultivate relationships and “allocate” coveted pieces to loyal clients, fostering a loyal following (and avoiding flippers). This model yields high revenue visibility (the waitlist can be several times annual sales for certain models) and minimal need for working capital (almost every Rolex that arrives is pre-sold or has a queue of buyers). In sum, WOSG behaves less like a traditional retailer and more like a franchise arm of the top Swiss brands, with economic characteristics that many consumer companies would envy.

History & Timeline

WOSG’s journey has a few pivotal chapters beginning with a Private Equity Turnaround from 2013–2018. Under Apollo’s ownership, Brian Duffy’s strategy of investing in upscale store refurbs and new openings (versus cutting costs) reignited growth. WOSG refocused on luxury watches, upgraded stores and systems, and expanded prime locations. WOSG acquired Mayors in 2017, marking its entry into America, and by 2019, UK luxury watch share had grown to 35% leading Rolex distribution by agencies and sell out—capabilities built over decades.

Sales and EBITDA had doubled leading up to its 2019 IPO and WOSG quickly proved its resilience – during COVID lockdowns, despite stores being closed for months, WOSG grew sales by shifting to appointment-based and online selling. The company also opened 8 new U.S. stores in late 2020, capturing pent-up demand. The stock rallied from the IPO to an all-time high around £16 in late 2021 as luxury watches saw an unprecedented surge in demand and secondary-market prices, fueled by asset price inflation and social media hype. The market then corrected sharply as prices for some Rolex models that traded 2× MSRP in the grey market fell back toward retail, and volume growth paused. In tandem, Rolex’s acquisition of Bucherer in August 2023 was a shock to investors sending shares ~ 30% lower in one day, ultimately bottoming around £3, a three-year low.

WOSG’s management has a proven M&A track record. The 2017 Mayors acquisition (for ~$105M) gave WOSG a foothold in the U.S. with 17 stores, which they grew to 30+ and turned Mayors into a platform for further Rolex network build-out. By all accounts, that deal was a success (WOSG U.S. is nearly £800M revenue). More recently, in 2022 they acquired Betteridge (a small U.S. jeweler with 4 Rolex doors) – that added presence in Greenwich CT, Aspen, and Florida. Within a year they refurbished Betteridge’s stores and integrated systems. These acquisitions have been smoothly absorbed, evidenced by U.S. margins holding up and increasing allocations to those doors.

In late 2022, Rolex launched a certified pre-owned program, authorizing select retailers to sell Rolex-backed used watches, opening a new growth vertical and signaling continued trust in WOSG to execute such a program. WOSG rolled out Rolex CPO in the U.S. and the U.K. in July and September 2023, respectively. Early results have been very strong – total pre-owned sales have grown to ~ 5-10% of group revenue in the first two years - expanding WOSG’s addressable market, profit pool, and pricing power (pre-owned pricing is set by the retailer and generally sells for a 25% premium to secondary prices).

Management announced an updated Long Range Plan (LRP) in November 2023 targeting a double in revenue to £3 billion and more than a double in operating profit by FY28. To achieve this, they earmarked a cumulative £350–500M through FY28 for acquisitions (self-funded via cash flows) to continue consolidating the U.S. and to enter Continental Europe (WOSG opened its first showrooms in Europe proper in 2022 in Sweden and Ireland, and acquired some Rolex doors in Denmark in 2023, before exiting the region). Recent acquisitions of Roberto Coin Inc. (exclusive distribution across North America and Caribbean) and Hodinkee (editorial, insurance, limited editions) add vertical jewelry capability and the world’s largest watch enthusiast media funnel—broadening growth vectors beyond primary watch sales and strengthening digital distribution.

Source: Federation of the Swiss Watch Industry

Industry Overview

The luxury watch retail industry represents a distinctive segment within the broader retail landscape, serving as the critical bridge between prestigious watch manufacturers and discerning consumers, operating through a complex network of authorized dealers, independent retailers, and increasingly sophisticated digital platforms. As understanding these industry dynamics is key to the investment thesis, we have dedicated considerable resources to this section of the report.

We encourage investors to review this material thoroughly, but have attempted to summarize the key takeaways below, for those inclined to move onto the next section, where we detail the current investment opportunity.

Key Takeaways

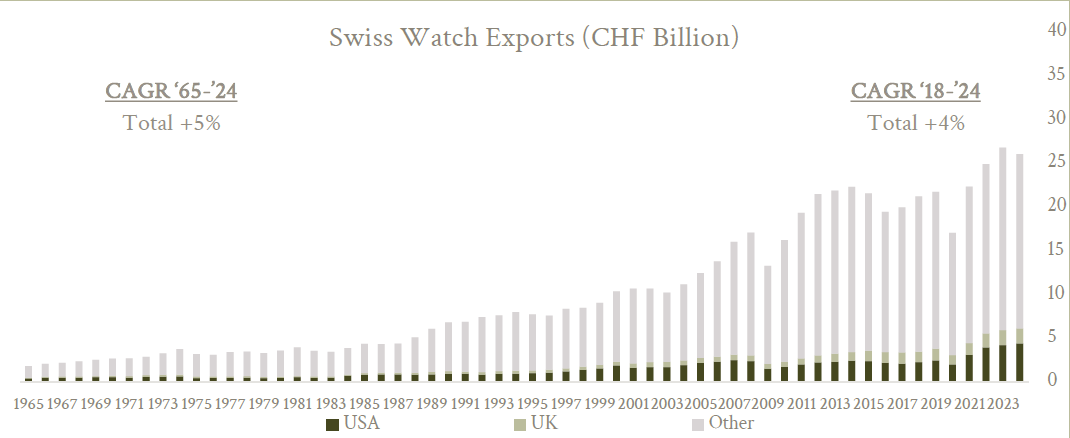

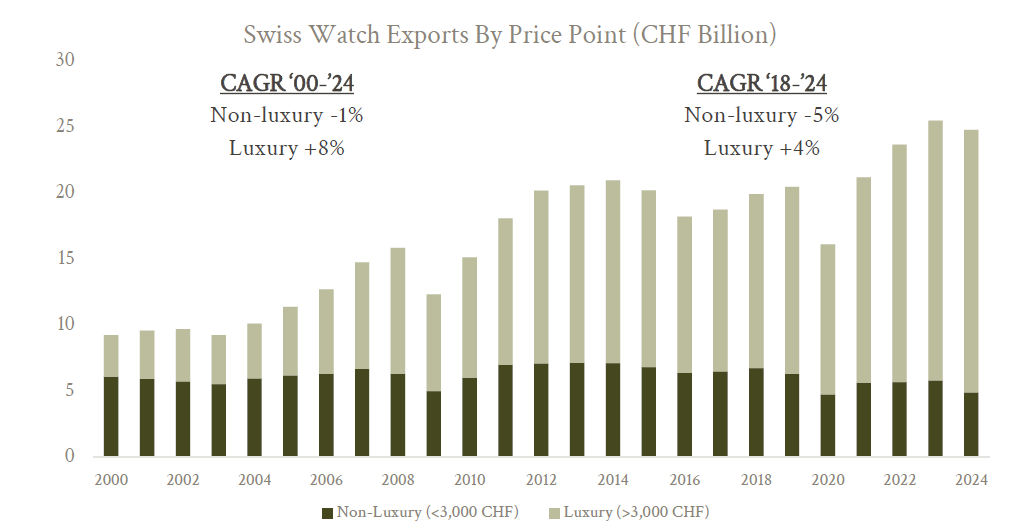

• The global Swiss watch retail market reached ~25 billion CHF in 2024, demonstrating substantial economic significance with a 24-year CAGR of +4.2% from 2000 to 2024 driven by premium pricing rather than volume growth. The Luxury watch segment (>3,000 CHF Price Point) makes up ~20 billion CHF of that total and grew +8.0% over the same period.

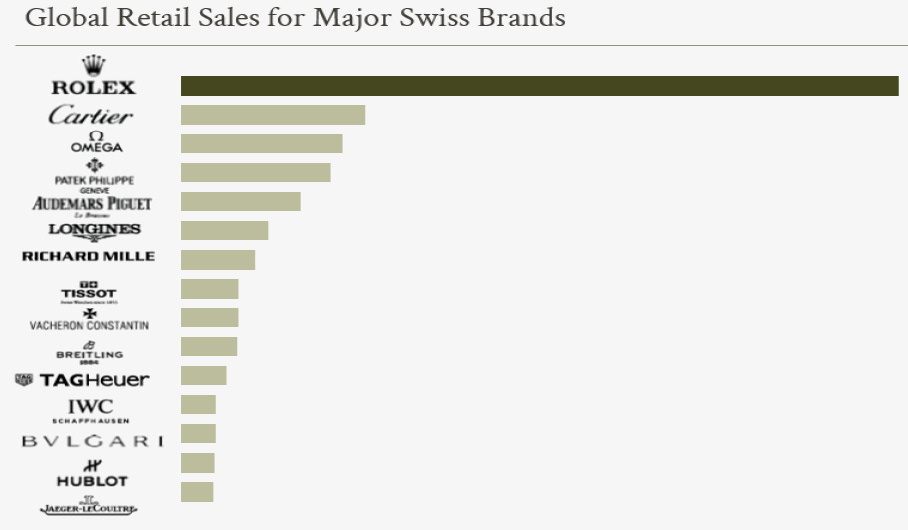

• The “Big Four” private brands—Rolex, Patek Philippe, Audemars Piguet, and Richard Mille—control 47% of Swiss watch market share while capturing 67% of industry profits.

• The industry maintains exceptionally high barriers to entry through selective distribution agreements requiring years of experience and category expertise, creating limited threat from digital pureplay development as brands require showroom approval for online selling.

• The certified pre-owned market is experiencing explosive growth and is expanding at ~ 5X faster than the primary market.

• Structural supply constraints from Swiss manufacturers create persistent supply-demand imbalances, driving customers to pre-owned alternatives, supporting premium pricing across the ecosystem.

Key Industry Characteristics

The luxury watch retail industry is undergoing a significant transformation shaped by enduring brand relationships, constrained production, and expanding global demand led by the U.S. market. These developments are reshaping how retailers like WOSG operate and compete in an increasingly dynamic market, yet the industry is distinguished by several unique characteristics that differentiate it from other retail sectors.

High barriers to entry, through Selective Distribution Agreements demand years of and expertise.

Strong value retention, supported by rarity, heritage, and craftsmanship, with products as investments.

Limited threat from e-commerce as brands require prior approval as a prerequisite for online sales.

Specialist expertise for manufacturers and retailers, as consumers demand authority and heritage.

Little inventory risk and high turnover, as top brands are generally presold with long waiting lists.

Overall market demand that exceeds production levels, given limited supply availability.

Market Map

The luxury watch retail ecosystem operates through a complex network of interconnected players, each capturing value at different points in the distribution chain, with clear market leaders emerging across different geographical regions. The market has undergone significant consolidation and vertical integration at both the manufacturing and retail levels, creating distinct competitive dynamics, as leading brands seek greater control over their distribution channels while retailers adapt through strategic acquisitions and diversification.

Brand Manufacturers: The “Big Four” Domination. The luxury watch landscape is dominated by the “Big Four” private brands: Rolex, Patek Philippe, Audemars Piguet, and Richard Mille, which collectively control 47% of the Swiss watch market share and capture 67% of industry profits. At the group level, four major conglomerates control the industry: Swatch, Rolex, Richemont, and LVMH, together account for over ~75% of total sales. Rolex stands as the undisputed market leader, with a commanding 33% retail market share, illustrating a level of dominance unparalleled in luxury goods.

Authorized Dealer Network. The authorized dealer channel represents the largest and most significant segment, operating under Selective Distribution Agreements that brands use to actively manage their distribution networks. These retailers maintain exclusive relationships with luxury watch manufacturers and are subject to strict operational standards and client experience requirements. Importantly, the retail market for luxury watches remains fragmented, predominantly comprised of a large volume of small retailers, as Rolex has steadily rationalized its agency numbers in both the US and UK over the past decade. This consolidation reflects brands’ push toward tighter control and fewer but higher quality touchpoints. WOSG stands as the largest multiband luxury watch retailer, operating 208 showrooms globally as of April 2025. In terms of scale and brand relationships, WOSG demonstrates significant competitive advantages. The company maintains partnerships with virtually all major luxury watch brands, with Rolex comprising over half of revenue. Bucherer represents another major retail player, particularly following Rolex’s recent acquisition of the Swiss retailer, marking a turning point in Rolex’s distribution strategy, as the brand previously had no direct-to-consumer exposure.

Brand-Owned Retail. Luxury watch brands are increasingly shifting toward direct-to-consumer retail models. The top private luxury brands control a large share of Swiss watch sales but capture an even larger share of profits with mid-30s operating margins. This concentration demonstrates the power of controlled distribution. Audemars Piguet has eliminated third party authorized dealers, operating exclusively through internal boutiques. Patek Philippe continues to cull its authorized dealership base, while brands prioritize limited edition and exclusive pieces for their own boutiques over authorized retailers, allowing them to capture both wholesale and retail margins while maintaining tighter control over customer relationships and brand presentation.

Online and Digital Platforms. Online Platforms have emerged as a critical component of the luxury watch ecosystem, representing a growing but carefully controlled segment, as major brands require prior showroom approval as a prerequisite for online selling, making multi-channel the preferred direction rather than pure digital retail. Chrono24 dominates as a primary online platform for watch sales, while eBay remains a significant but less premium option for luxury timepieces. The secondary market is growing considerably faster than the primary market. Hodinkee represented the leading digital editorial content provider before its acquisition by WOSG in October 2024. This acquisition included editorial, insurance, and limited-edition businesses, strengthening WOSG’s online leadership position. The integration allows WOSG to leverage Hodinkee’s influence in the watch enthusiast community and its ability to secure exclusive limited editions from major brands.

Preowned and Secondary Market. The preowned watch market has become increasingly sophisticated, with specialized platforms capturing significant value. Bezel operates a pure marketplace for preowned watches in the US, handling everything from sub $1,000 pieces to watches exceeding $1 million. Most watches trade below retail on the secondary market except for highly sought-after brands like Rolex, Patek Philippe, and Audemars Piguet. WOSG has built a significant preowned presence through its acquisition of Analog/Shift in 2020 and the development of Rolex CPO programs. Retailers often achieve higher gross profit dollars on preowned watches than new pieces, making this segment particularly attractive. Richemont acquired Watchfinder in 2018, while WatchBox became part of the 1916 Company, demonstrating the strategic value of preowned operations.

Auction Houses and High-End Specialists. Auction houses including Sotheby’s and Christie’s occupy a specialized niche focusing on unique, one-of-a-kind watches and significant collections rather than everyday luxury timepieces. These platforms primarily serve collectors seeking rare or vintage pieces rather than competing directly with retail channels for contemporary models.

Competitive Landscape

The luxury watch retail sector combines elements of both fragmentation and oligopoly, creating a unique competitive environment characterized by intense brand dependency and high barriers to entry.

Market Structure Dynamics. The retail landscape operates as a highly fragmented market with only a small number of market leaders and a long tail of independent distributors. However, this fragmentation masks an underlying oligopolistic structure at the brand level, where the top private luxury brands control a large share of Swiss watch sales while capturing a disproportionate share of industry profits. The US market exemplifies this fragmentation, representing an estimated ~$4.4 billion retail opportunity where WOSG commands a high‑single‑digit share, while ~ 70% of the market is still comprised of mom and pop jewelers with one to three stores.

Key Competitive Advantages. Brand Relationships represent the most critical competitive differentiator in luxury watch retail. Distribution operates under strict Selective Distribution Agreements (SDAs) that are granted on a store-by-store basis and actively managed by brand owners. These legal agreements include stringent requirements around price policy, distribution channels, presentation standards, and customer experience. Location and Customer Experience serve as secondary competitive advantages, as evidenced by the industry’s emphasis on destination showrooms and the requirement for showroom approval as a prerequisite for online selling. The sector remains specialist oriented, where consumers respond to expertise, authority, and heritage. Scale benefits provide negotiating leverage, particularly with less prestigious brands that trade at discounts to the secondary market and actively seek placement in major retailers. This scale also enhances brand trust and customer awareness compared to smaller independent dealers.

Barriers to Entry. The luxury watch retail sector maintains exceptionally high barriers to entry, driven by the requirement for strong brand partnerships built over many years of experience and category expertise. Brands actively manage distribution through SDAs, creating a controlled ecosystem that limits new entrants. Capital requirements for establishing premium retail locations and maintaining brand-compliant showrooms represent significant financial barriers. Additionally, the relationship-based nature of brand partnerships means new entrants face substantial challenges in securing desirable brand allocations, particularly from top tier manufacturers like Rolex and Patek Philippe.

Supply Chain and Pricing Dynamics. The luxury watch supply chain is characterized by managed scarcity, among the top private brands through controlled production and multi‑year waitlists on popular models. This scarcity model contrasts with traditional retail dynamics, where demand often exceeds supply for key products. Pricing strategies reflect this scarcity premium, with luxury brands achieving higher margins through restricted availability rather than volume sales.

Recent Consolidation Activity. The industry is experiencing significant consolidation driven by a strategic shift toward direct retail control. This trend reflects brands’ desire to bring more distribution inhouse, similar to Audemars Piguet’s strategy of operating exclusively through brand-owned boutiques. Tariff disruption and market dynamics are creating additional M&A opportunities, as independent dealers face pressure to sell while larger players like WOSG pursue strategic acquisitions at reasonable prices. The consolidation trend is evident in the reduction of single-door dealerships, with some operators losing multiple dealerships while others expand their footprint. This evolving competitive landscape suggests a bifurcated future where scale players with strong brand relationships will gain market share, while smaller independent dealers face increasing pressure from both brand consolidation strategies and operational challenges in maintaining competitive positioning.

Value in the luxury watch ecosystem is heavily concentrated among the leading brands and their preferred retail partners. The top private brands achieve high profit concentration through tight channel control and selective distribution, supported by managed scarcity and multi-year waitlists. Retailers have faced margin pressure over time as Swiss watch brands have reduced retailer margins from over 50% to 35% - 45% currently, depending on brand strength. However, retailers can capture additional value through services, preowned sales, and exclusive partnerships. The most successful retailers like WOSG maintain strong relationships with multiple brands while diversifying into complementary areas like luxury jewelry, servicing, and digital media. Recent strategic moves reflect the industry’s consolidation trend and brands’ desire for greater control. Beyond the major acquisitions mentioned, the market has seen continued investment in flagship locations, mono-brand boutiques, and digital capabilities as players position for long term growth in an increasingly consolidated ecosystem.

Source: Federation of the Swiss Watch Industry, Morgan Stanley Research, Richemont, Swatch, LVMH

Market Structure

The Swiss luxury watch market is structurally concentrated: the “Big Four” (Rolex, Patek Philippe, Audemars Piguet, Richard Mille) control an outsized share of industry value and an even greater share of profit, with Rolex alone at ~33% retail share in 2024. The model is further advantaged by selective distribution (brands tightly control doors, product, and presentation) and chronic supply scarcity supporting full price sell through, low obsolescence risk, and attractive unit economics.

Brands use selective distribution agreements that cap door counts, enforce exacting standards and client experience, and create high barriers for new entrants. Retailers must prove expertise and invest at brand standards to earn allocations, favoring scaled specialists like WOSG.

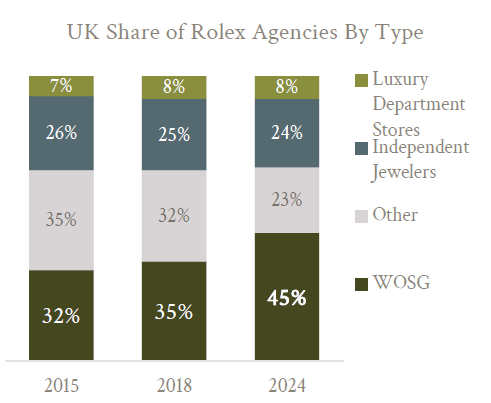

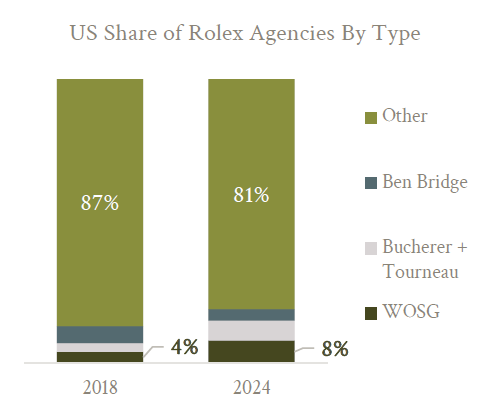

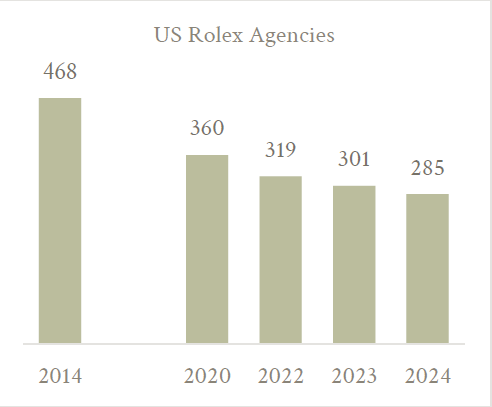

The luxury watch distribution model is unlike typical retail – brands do not sell direct online or via their own shops (with a few exceptions), instead relying on a global network of authorized dealers (ADs) for sales and service. For Rolex and peers, preserving brand prestige and pricing power is paramount, supply is tightly controlled, and retail partners are chosen extremely carefully, resulting in an oligopoly-like dynamic in each region, with a handful of long-established retailers granted dealerships and often protected by territory. In the UK, WOSG is by far the leader, followed by smaller chains like Bucherer UK (~ 5% share) and a few independents. In the U.S., distribution is highly fragmented – Rolex had ~ 2,000 U.S. AD doors in 2008, now fewer than 300 – and WOSG’s entry via acquisitions has made it the largest player.

Source: Source: Federation of the Swiss Watch Industry, Watches of Switzerland, Rolex

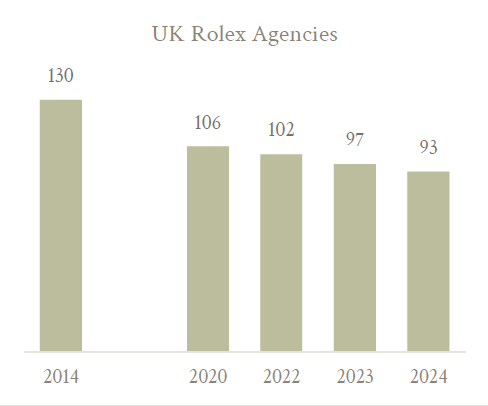

The trend is consolidation: brands are reducing the number of retail partners and allocating more volume to a few “trusted, well-capitalized” retailers like WOSG. This is evidenced by Rolex culling its UK AD count from 130 stores in 2014 to 93 by 2024 – smaller family jewelers are being phased out in favor of players that can invest in spectacular boutiques and service quality. WOSG’s ability to pour millions into renovating flagship stores (e.g. turning a 900 sq ft shop into an 8,000 sq ft Rolex temple on Bond Street) is unmatched by mom-and-pop rivals, giving it an enormous scale advantage.

In the U.S., we expect a similar pattern: WOSG is targeting top cities for Rolex-led flagship stores, and Rolex is likely to reallocate supply toward those few preferred partners and away from under-invested small dealers. Competitively, aside from Bucherer and a few regional chains, WOSG’s main “competitors” are the luxury brands themselves, with some high-end brands (e.g. Audemars Piguet, Richard Mille) reducing third-party distribution to favor their own boutiques. But even in those cases, WOSG often operates the boutique as a partner (for AP) or remains a key multi-brand seller.

Overall, given decades-long relationships (WOSG has been an AD of Rolex since 1919, Patek Philippe since 1960s, etc.) and its impeccable execution, WOSG’s competitive position is virtually unassailable benefitting from first-mover advantage in consolidating a large, under-penetrated market. Scale enables faster inter store sourcing, better inventory turns, and showroom capex amortized over more revenue—capabilities smaller rivals struggle to match.

Source: Federation of the Swiss Watch Industry, Watches of Switzerland, Rolex

Secular Trends & Outlook

The luxury watch market has proven resilient and growing over time. Global high-end watch sales have grown at a high-single-digit CAGR for decades, driven by regular price increases rather than unit volume, with mix continuing to premiumize (pieces > CHF 50K represent a disproportionate share of value and growth despite tiny unit share).

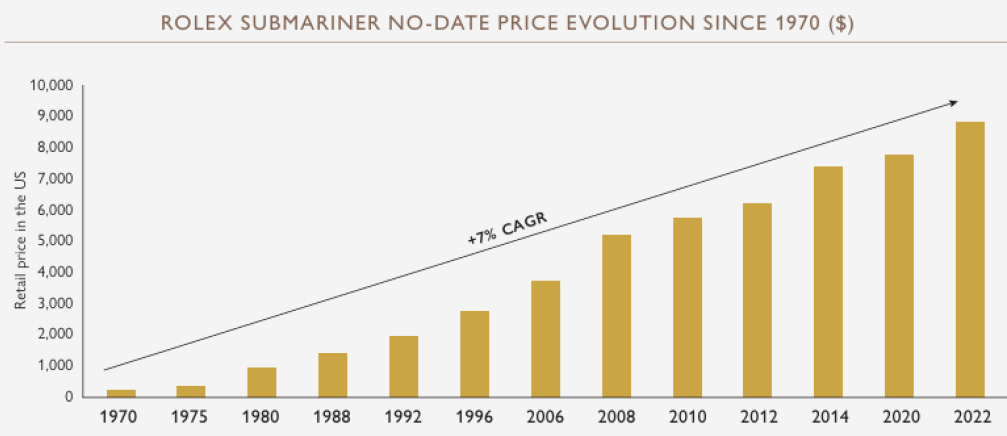

True luxury watches are timeless assets passed down for generations, with persistent demand fueled by scarcity and craftsmanship. As one industry adage goes, for collectors “if you have 2 you want 4, if you have 5 you want 15”. This inelastic demand allows brands to raise prices even through recessions (Rolex raises prices annually), and never discounts – models often sell at a premium on the secondary market. Importantly, the top end of the market (where WOSG is focused) has been immune to the smartwatch trend impacting lower-end timepieces.

Selective distribution, production discipline (especially at the Big Four), and brand control of placements underpin ASP growth and rarity value, which moderates cyclicality versus most discretionary categories and supports gross margin resilience at the retail level.

Source: Federation of the Swiss Watch Industry

The Certified Pre-Owned (CPO) market has emerged as a major growth driver for the industry as scarcity drives customers toward pre-owned alternatives. The move to pre-owned accelerated further after becoming institutionalized via Rolex’s rollout of its own CPO program in 2022–23 (WOSG is a key partner). Seemingly overnight, Rolex legitimized pre-owned sales at Authorized Dealers, driving incremental volume (people trade up more easily) and profits (CPO inventory carries higher markups set by the retailer), with the pre-owned market growing multiple times faster than primary sales, and by some estimates, already comparable to primary sales in the U.S. While short-term cycles occur (as seen in 2023’s correction from 2021’s frenzy), the structural drivers – limited supply, rising global wealth, price inflation – remain intact. Retailers are adapting through improved inventory management and omnichannel strategies that blend physical and digital experiences, while focus shifts toward inventory turns and showroom productivity as key performance indicators.

For WOSG, this environment is ideal, as it yields full-price sell-through and high inventory turn, while widening the funnel for first time clients and recapturing value that once leaked to grey channels. The company’s strategic acquisitions of Analog/Shift (vintage dealer) and Hodinkee (pre-owned marketplace) position it well to capitalize on this trend, potentially reaching ~20% of total Rolex revenue in the coming years.

Luxury watch e‑commerce is maturing, but brands generally require showroom validity before online selling—limiting pure‑play digital disruption. The winning formula is “omni” (showroom + digital clienteling), not “online only.” WOSG’s acquisition of Hodinkee for £10.7 million in October 2024 represented a strategic move to strengthen its digital capabilities, providing access to a large base of annual website views and total active users across digital platforms, to leverage content-driven sales and reduce customer acquisition costs while expanding online market presence.

Despite digital growth, the importance of physical retail experience remains paramount for luxury watch sales. Industry experts emphasize that client engagement, storytelling, and product knowledge are critical differentiators for retailers. The combination of luxury goods plus experience in mono-brand boutiques proved particularly successful during the post-pandemic recovery. Brand partnership management has become increasingly sophisticated, with retailers needing to balance online and offline channels while respecting brand distribution policies. Top brands, like Rolex, maintain restrictions on online sales of new watches, requiring careful channel management.

Why The Opportunity Exists

WOSG’s durable access to Rolex and top maisons, advantaged U.S. consolidation runway at attractive incremental returns, and scaling Rolex CPO/services flywheel create compelling risk-adjusted compounding from a depressed single-digit multiple as tariff noise fades and operational momentum compounds. The stock’s derating reflects a sequence of narrative blows that compounded into a “structural risk” story.

The prevailing narrative paints the company as an “ex-growth luxury middleman at risk of obsolescence” leaving shares at a steep discount to both luxury brands and specialty retailers. The bear case assumes 1) structural erosion from Rolex–Bucherer verticalization; 2) cyclical demand risk and a fading U.S. runway for a low-growth retailer reliant on a single supplier; and 3) tariff-driven margin damage. We believe these concerns are flawed or transient, and think the current valuation overly penalizes shares.

Our differentiated view: allocations to top-performing partners are stable and consolidating in WOSG’s favor; tariffs are largely a gross‑margin mix event absorbed through price/margin sharing; and U.S. growth should accelerate via consolidation, and rapid expansion of Rolex CPO.

Misperception I: Bucherer Acquisition Portends Disintermediation

Rolex’s acquisition of Bucherer catalyzed a perception that retail brand partners could be disintermediated, despite brand statements to the contrary and subsequent trading evidence. Buy side and expert calls captured this skepticism repeatedly, with skeptical investors probing allocation dependence and the waitlist model’s durability. In the meantime, the market keeps discounting allocation risk as a structural overhang, assigning a permanent handicap to WOSG’s multiple.

Broyhill Take: We believe this was a knee-jerk interpretation that doesn’t withstand scrutiny. Selective distribution is foundational to the category and WOSG’s decades-long execution, elevating brand standards at scale, make it strategic infrastructure for top maisons. Brands have tightened, not expanded, door counts, becoming increasingly reliant on a small number of exemplary partners to cover markets and client experience. The continuation of announced Rolex projects with WOSG and the rollout of Rolex Certified Pre‑Owned across WOSG’s estate post the Bucherer acquisition indicate ongoing partnership depth inconsistent with consensus concerns. The post Bucherer reality has not produced a wholesale shift away from top-tier partners. Instead, brands continue pruning doors and leaning into a few trusted retailers. WOSG’s scale, estate quality, and data make it more, not less, valuable today.

We believe Rolex’s acquisition of Bucherer was a one-off event to secure a legacy Swiss partner, not a strategic shift to owning retail. Rolex and WOSG have a 100+ year relationship and Rolex has encouraged WOSG’s growth (one industry advisor highlighted Rolex’s emphasis on long‑term partnerships while suggesting that WOSG management would not have guided aggressively without allocation support). Notedly, Rolex is run by a non-profit foundation with no incentive to chase retail profit. We also think it’s telling that Rolex chose not to rebrand Bucherer stores as “Rolex” and emphasized that they will continue to operate independently. Concentrating inventory in one captive retailer would be counterproductive: 20× more Rolex revenue flows through non-Bucherer dealers than through Bucherer, so tilting allocations heavily would alienate the global network and barely move Rolex’s needle. And with Rolex expanding production by ~ 60% by 2030, it will increasingly rely on retailers like WOSG to absorb that volume.

The notion of vertical integration at Rolex’s scale is unfounded and nonsensical – it would require decades and billions to replicate WOSG’s retail footprint, with huge operational risks and brand damage. Furthermore, Rolex historically acts to strengthen its best partners, not weaken them. It has systematically pruned smaller ADs (e.g. cutting U.S. doors from 2,000 to fewer than 260) which funnels more supply to top players like WOSG. In short, the fear of Rolex breaking up with WOSG is extremely low probability. Instead of displacing WOSG, Rolex’s actions indicate WOSG will continue to gain share – a view corroborated by both companies ongoing investments. While consensus worries about DTC displacement and WOSG allocation cuts, we see distribution being optimized and high‑performing partners, like WOSG, gaining share.

One former competitor thinks the risk of Rolex starving WOSG is “unfounded,” highlighting Rolex’s slow, methodical channel moves, lack of shareholder pressure, and a long‑standing preference for “master franchise” partners; any incremental benefit to Bucherer is unlikely to come directly at WOSG’s expense. Another former executive notes that brands retain an interest in strong third‑party partners with national scale, such as WOSG, to sustain distribution breadth. Experts emphasize the scarcity of high-quality platforms and the accelerating consolidation wave, elevating strategic value beyond retail comps.

Misperception II: Industry Digestion & Fading Runway

The abrupt end of the luxury watch boom in mid-2022 led to a narrative that demand had been pulled forward and that the market could be in for an extended slump.

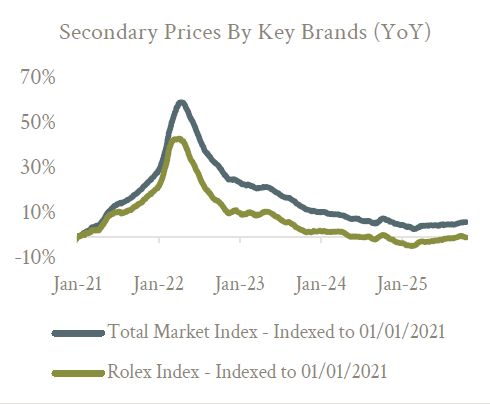

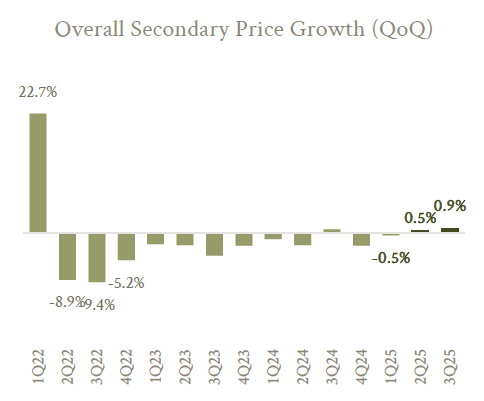

Broyhill Take: Secondary market prices for Rolex, which overshot during the bubble, have normalized to historical premiums over retail (a sign that the excess froth is out). Volumes have plateaued, not collapsed and Swiss exports to the U.S. continue to grow, while Rolex waitlists remain lengthy. Notably, luxury watch sales tend to be more supply-constrained during downturns: brands like Rolex pull back shipments to avoid oversupply, effectively putting a floor under retail pricing (Rolex did this in late 2022). WOSG’s UK revenue dip should be viewed in this context: it followed several years of above-trend growth (UK sales +38% from FY19 to FY22) and was exacerbated by a tourist spending headwind. The UK’s elimination of certain tourist shopping incentives in 2021 reduced international visitor spending, particularly affecting London luxury retailers. Before Brexit, tourist shopping, especially by Chinese and Middle Eastern visitors, was a significant component of UK luxury sales. Yet underlying domestic demand remains intact (with potential upside should those incentives return to London), and UK softness is more than offset by U.S. strength, which is already nearly half the business.

Bottom line: we believe the post-COVID hangover in watches is largely behind us, current trends are already improving, the “air pocket” in UK demand appears transient, and the long-term growth vectors remain intact.

Source: WatchCharts

Another argument we’ve heard is that because WOSG is essentially an agent for Rolex, it deserves a low multiple akin to an auto dealer or franchised distributor, given the theoretical “one supplier” risk. While we acknowledge WOSG lacks full control over product supply, the quality and durability of its cash flows far exceed that of a typical retailer. WOSG enjoys many traits of a luxury brand without the heavy R&D or marketing spend. Its revenue is not “one-off” transactional in nature but rather relationship-driven and recurring (clients buy multiple watches over years). As long as Rolex and others choose to distribute via third parties – which they’ve done for over a century – WOSG’s business is effectively an extension of those brands. It is more protected than a typical franchise because Rolex cannot simply license anyone new (they would risk brand damage by expanding doors recklessly). One could argue WOSG should trade closer to luxury brand multiples than to commodity retail. We’re not suggesting parity with Hermes, but a valuation in line with dying departments stores or slow growth supermarkets seems even more absurd.

As the dust settles and fundamentals speak for themselves, we believe investors will come to understand that this is not an impaired business model. Instead, allocation continuity to a scaled, standards‑led partner anchors high‑visibility, waitlisted revenue, while distribution consolidation creates incremental share opportunities at attractive economics. WOSG is set to benefit from a rationalizing U.S. store network with smaller independents (roughly 70% of the market) retrenching, opening the door for scaled operators with strong client lists and shop‑fit standards. And WOSG remains far ahead of the competition on omnichannel innovation and brand‑boutique operations, while CPO widens the profit pool, deepens client relationships, expands the addressable market, and drives trade‑in attach.

Misperception III: U.S. Tariffs and Margin Squeeze

US tariff policies represent a significant potential headwind. The initial U.S. tariffs of 10% on Swiss watches created the potential for up to 100 bps of margin pressure for WOSG, depending on how brands divided incremental costs between manufactures, retailers and consumers.

To date, the pricing reaction has varied significantly by brand, with Patek Philippe raising prices by 15%, other top brands raising prices in the mid-single digit range, while Rolex has yet to implement a tariff-driven price increase (after already raising prices twice earlier in the year). If current tariffs hold at the threatened 39% rate, investors worry that brands would hike prices further with associated volume risks, and additional pressure on retail profit margins

Broyhill Take: Tariffs are a policy risk, but the industry’s playbook is pricing power. Swiss watch exports to the U.S. spiked >100% in April and into the summer as brands positioned inventory ahead of tariff uncertainty - most brands have already adjusted margin splits and pricing. Industry participants expect a “shared‑pain” outcome across price, brand margin, and, to a lesser extent, retailer margin; high‑ticket, waitlisted SKUs show low elasticity, limiting volume risk at the premium end. Recent commentary from Swatch flagged this limited elasticity to initial price increases, suggesting pass‑through can be absorbed without a step‑function demand break at the top end.

We expect limited volume impact from WOSG’s top brands (~ 80% of sales), with any hit to demand concentrated in non–supply‑constrained brands. Core demand is largely inelastic with any P&L impact mainly on gross‑margin mix and gross profit neutral after price hikes. Meanwhile, recent comments from management point to “consistently strong” U.S. trading despite tariffs into late August and a reiterated outlook that the current FY26 guidance is on track. Notably, about half of group sales are waitlisted products, providing visibility and cushioning cyclicality, while WOSG’s margin structure is inherently scalable and should expand over time. The fastest-growing pieces of the business are in the U.S. providing a natural mix shift towards higher margin sales, with accelerating categories like pre-owned expected to grow twice as fast as primary sales.

Source: Rolex, Google Images

In short, the price today embeds low‑growth, low‑margin mid‑cycle economics, broad U.S. demand risk, and structural channel-share loss that the data does not corroborate. The distribution of outcomes points to ongoing allocation stability and an accretive and accelerating mix towards the US and CPO, which should allow valuation to mean‑revert toward historical anchors as uncertainty clears.

Investment Thesis

Our investment thesis rests on three core pillars summarized below and detailed at length in the following section of this report.

The Moat. Privileged, long-standing relationships with the most coveted Swiss watch brands secure privileged inventory, shield WOSG from online competition, and confer scale advantages unavailable to smaller, independent retailers.

The Runway. An underpenetrated and fragmented U.S. market represents a multi-year reinvestment runway at attractive returns on capital, with upside from the rapid growth of Rolex Certified Pre-Owned sales, already the second largest brand at WOSG.

The Mispricing. Shares are priced like a no-growth cyclical retailer, despite a business that operates as a luxury brand partner, creating an usually wide disconnect between perception and reality, with several catalysts to unlock value on the horizon.

Investment Thesis Point I: The Moat

Unique, long-standing partnerships with the most coveted Swiss watch brands give WOSG superior access to constrained inventory, insulating revenues and margins through the cycle. WOSG’s economics are anchored by an unusually close, “quasi-subsidiary” relationship with Rolex and top brands that secures privileged inventory, shields it from online competition, and confers scale advantages unavailable to other retailers.

For more than 75 years the Group has cultivated trusted relationships with Rolex, Patek Philippe, Audemars Piguet and other top maisons; top brands account for over three quarters of sales and purposely limit distribution, keeping industry supply well below demand and sustaining pricing power.

Because allocations drive sales almost 1-for-1 and carry stable gross margins, WOSG benefits from high barriers to entry, limited competitive encroachment, and resilience when macro conditions soften. Rolex sells only through authorized distributors and treats WOSG as one of its most trusted partners, providing product on consignment with no inventory risk and granting allocations that competitors cannot match; this dynamic means WOSG effectively benefits from Rolex’s brand strength while avoiding the capital intensity of manufacturing.

Enduring supply-demand imbalance in Swiss luxury watches underpins pricing power and resilient volume growth. A long runway in the U.S., plus Rolex CPO adds new, high‑quality growth vectors with operating leverage. Global demand for flagship Swiss brands materially exceeds supply, allowing WOSG to sustain premium pricing, steady sell-through and strong margins even in a normalizing macro backdrop. Key products remain on “Registration of Interest” lists signaling healthy wait-lists despite successive price increases.

Limited capacity expansion at the Swiss maisons, coupled with high input costs, supports long-term price inflation, protecting WOSG’s gross margin while cushioning volumes in softer cycles.

Investment Thesis Point II: The Runway

An under-penetrated U.S. market offers the largest single growth vector, with store openings and mono-brand boutiques set to accelerate share gains. Management has already proven the playbook through acquisitions and flagship boutiques, while brands curtail distribution to rival retailers, effectively transferring share to WOSG. Given that the U.S. is the world’s largest market for Swiss watches, incremental square footage and brand allocations can drive outsized top-line growth.

A normalizing luxury-watch cycle and an underpenetrated U.S. market create a multiyear runway for high-return reinvestment that the market is overlooking. Secondary-market premiums and WOSG margins have largely normalized, while Swiss watch exports per capita in the U.S. are half those of the UK. Replicating its UK playbook in a fragmented U.S. landscape of mom-and-pop retailers allows WOSG to deploy capital at attractive returns., adding a large, fragmented profit pool to the portfolio. Since entering the market in FY18, WOSG has compounded U.S. revenue at 36.3% CAGR, surpassing £750 million in FY25 and shifting the regional mix to the U.S. The group has leveraged showroom relocations, mono-brand boutiques, and targeted acquisitions to capture share in what management calls “the clear #1 market globally” for luxury watches. With only 60 doors open versus hundreds of potential locations and a market still dominated by independents, runway remains significant.

Continued door expansion, omni-channel integration and entry into CPO and luxury jewelry position the U.S. as WOSG’s primary growth engine for years to come. Beyond new-watch sales, WOSG is scaling higher-margin adjacent businesses and after-sales service. These initiatives smooth cyclical risk and enhance customer lifetime value while preserving balance-sheet flexibility This blend of organic and inorganic growth, underpinned by strong cash conversion, supports the prospect of continued long-term compounding for shareholders.

We think Rolex CPO, which launched in 2023, is a game-changing program, allowing WOSG to sell pre-owned Rolex watches with an official Rolex certification/warranty. This program effectively unlocks huge secondary market demand (previously served only by grey dealers) allowing WOSG to monetize trade ins and upgrades, at robust margins and higher absolute gross profit dollars per watch. Importantly, successful rollout of CPO can boost both growth, while strengthening customer relationships (one-stop shop for new and pre-owned).

Performance of CPO is exceeding expectations with total pre-owned sales doubling YoY in Q4 – proof of huge demand that WOSG can profitably serve. Meanwhile, channel checks indicate repair capacity has also doubled since the launch (an underappreciated medium‑term margin stabilizer) to support throughput. And pre‑owned is already WOSG’s “second biggest brand” after Rolex (~ 85 - 90% of pre‑owned volume is Rolex), representing 5-10% of group sales with 100% of WOSG’s U.S. Rolex agencies authorized (vs. ~39% of US agencies overall).

We see potential for CPO to reach ~20% of Rolex sales as pricing power turns drives higher gross‑profit dollars, with per‑door U.S. metrics already trending higher, reinforcing the leverage and underscoring structural economics. To put the scale in perspective, consider that multiple industry experts believe the secondary market for luxury watches is as large as the primary market (~$20B+ annually). So capturing even a slice of this rapidly growing market is material. Here, WOSG’s advantage is trust and physical presence – buyers of a $15K pre-owned watch may prefer an authorized retailer’s guarantee over an eBay listing. Rolex’s own motivation is similarly aligned: by channeling sales through ADs, they reinforce the value of buying from authorized sources.

Bottom Line: A long runway in the U.S. plus Rolex CPO adds new, high‑quality growth vectors with operating leverage. The U.S. market is structurally underpenetrated and distribution remains fragmented while WOSG has mapped the estate and is the only scaled consolidator building flagship‑grade doors that brands reward with growing allocations.

Investment Thesis Point III: The Mispricing

To quantify the draconian assumptions currently embedded in WOSG’s share price, we ran a reverse discounted-cash flow model to better understand implied expectations. In short, at <400 per share, the market is telling us that WOSG’s business model is subject to significant terminal risk. Using a 10% cost of capital and a 3% terminal growth rate, we estimate the market is discounting 0% revenue growth into perpetuity with shrinking margins, which appears “somewhat” pessimistic given WOSG’s historical track record (steadily improving operating margins driven by sales growth approaching 20% annually) and even bearish consensus expectations of mid-single-digit top-line growth.

While there is certainly a non-zero chance that the dynamics between Rolex and its key brand partners will shift in the coming years, particularly as Rolex integrates its acquisition of Bucherer, it seems that investors are valuing WOSG as if this is a forgone conclusion, despite a century of evidence to the contrary.

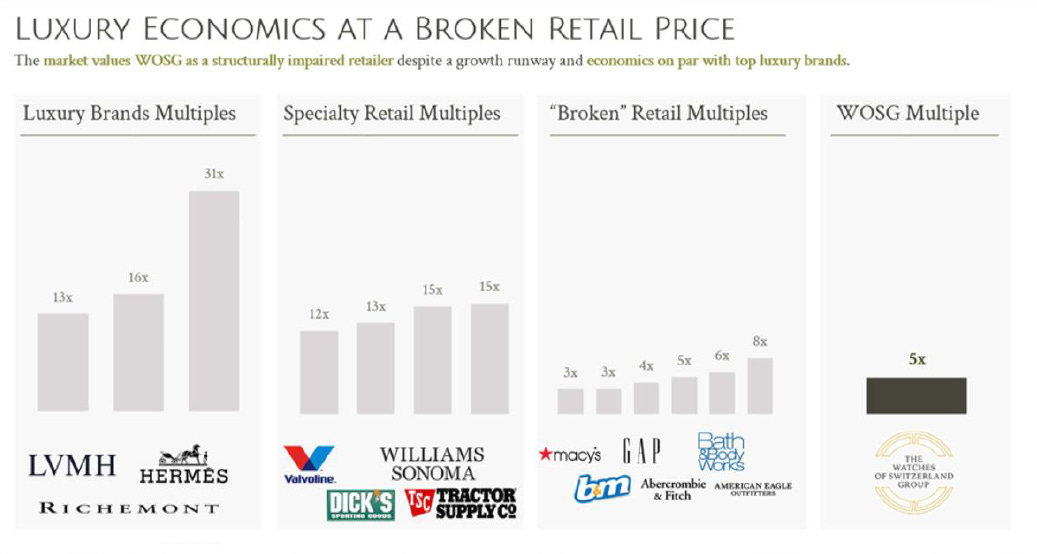

Expectations are abnormally low for a company of this quality - at just 5x EBITDA, the market is discounting a broken model despite evidence pointing to durable growth and multiple ways to win. Investors are currently pricing WOSG as a structurally impaired retailer despite a growth runway and economics on par with top luxury brands.

For comparison, consider that luxury brands trade at ~15-30x NTM EV/EBITDA while specialty retailers tend to trade in the mid-teens – we think somewhere in between these levels is the ideal valuation for WOSG. Precedent transactions of luxury watch and jewelry retailers over the past decade offer another valuation perspective and imply WOSG valuation from ~ £7 per share on an EV/Sales basis to ~£11 per share on an EV/Door basis.

Source: Bloomberg

A decade of compound growth, high returns on capital and balance-sheet strength sets up a valuation re-rating opportunity. Despite this growth shares trade around their 2019 IPO price even though revenue has more than doubled and EPS is up 4×. Management’s alignment—CEO owns 3.2 % of the equity and insiders have been recent buyers—reinforces confidence that ongoing execution can close the disconnect between fundamentals and market perception. We flush out our fair value estimates in greater detail in the following section.

Valuation & Key Assumptions

It is rare to find a consumer business with WOSG’s combination of visibility (backlog via multi-year waitlists), organic expansion (across a fragmented market), and reinvestment opportunities at high rates of return trading at such a low multiple. We believe this mispricing exists because investors are extrapolating the recent downcycle and exaggerating structural risks.

Three years into one of the worst downturns for the luxury industry, which has been particularly harsh for the Swiss luxury watch market, with shares already down ~ 75% from their prior peak, we see little downside at today’s price, with significant upside potential should the future unfold in a slightly more positive manner. In the following paragraphs, we outline our assumptions in modeling that upside potential, quantifying key drivers for the stock, examining our view vs consensus, and ultimately, the impact on valuation.

Organic Growth

WOSG revenue growth has increased at a 10%, 15%, and 16% rate over the past three, five, and ten years, respectively. Looking ahead, we see the key drivers of top-line growth as Rolex supply allocation (consolidating among its top retail partners), U.S. market expansion (WOSG market share in the US sits at a fraction of UK levels), continued pricing power for the top, supply-constrained brands (Rolex prices have increased at 7% annually for the past 50+ years), and the general demand environment for luxury watches. At the same time, Rolex Certified Pre-Owned is quickly becoming an increasingly important growth driver for the company, providing incremental growth on top of new watch sales, while providing a new avenue of client acquisition.

Source: Stifel Research, Rolex

Putting it all together, we model 3.5% - 12% annual top-line growth through FY29, with 7.5% growth our base case. While consensus estimates don’t look out quite this far, our upside scenarios (averaging our base and bull case assumptions) result in FY28 sales more than 11% ahead of the street and FY29 sales more than 20% ahead of the street, as analysts appear anchored to the current short-term trough and hesitant to forecast continued growth in Rolex allocations. In contrast, we see revenues accelerating into FY27-28 through a combination of new doors, market share gains, and increased pricing. We think consensus expectations dramatically underestimate how much share WOSG can seize in the U.S. as well as the tailwinds from dealer rationalization noted below.

Historical performance would appear to support our work as global Swiss watch exports grew at 4–5% annually for the past 20 years, with U.S. sales growing faster than the overall market and WOSG growth underpinned by aggressive shares gains. At the same time, 3% - 5% annual price increases on supply-constrained luxury brands would support the low end of our growth forecast without assuming any lift from unit growth. That seems highly unlikely in our opinion.

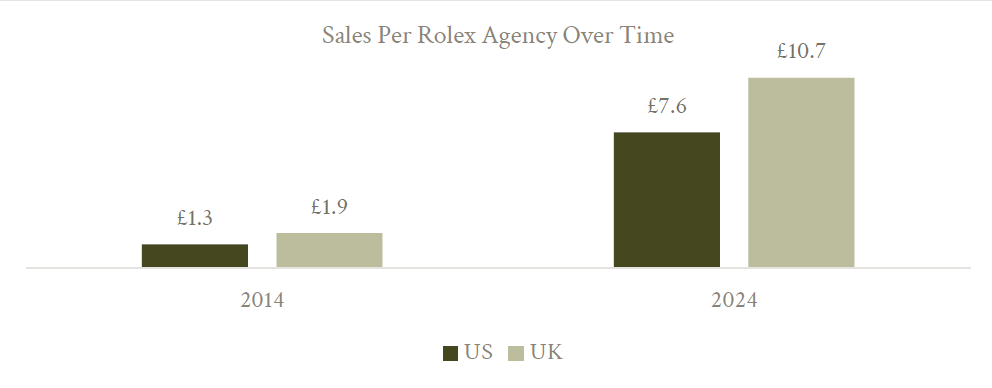

Even in a scenario where WOSG store growth ground to a halt, continued dealer rationalization in the U.S. should support very healthy sales growth. Consider that Rolex sales per agency in the UK have increased at more than a 19% clip from £1.9 million to >£10 million over the past decade as increasing Rolex sales were spread over a decreasing number of agencies. Should the U.S. follow a similar trajectory, continued consolidation alone would drive sales above the high end of our forecasts.

Source: Watches of Switzerland, Rolex, Morgan Stanley Research, Broyhill Asset Management Estimates

Margin Trajectory: Scale Economies, Mix, and Operating Leverage

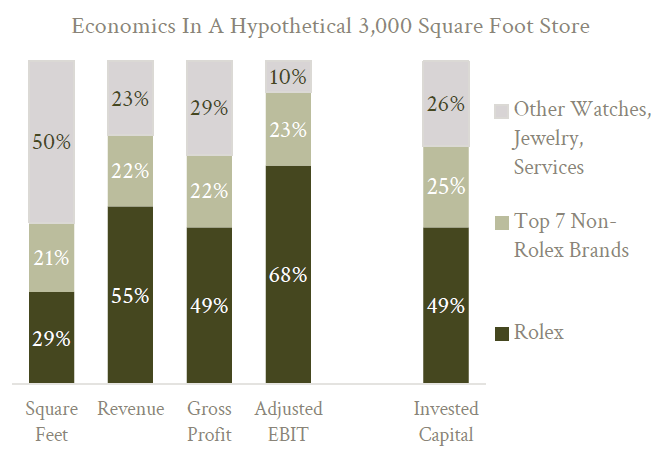

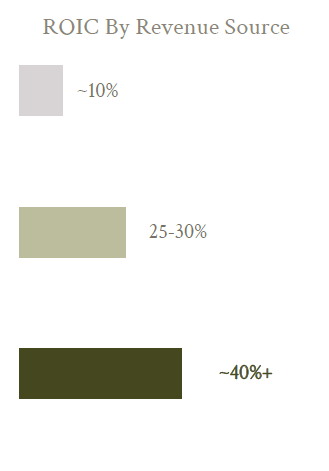

Over the past decade, WOSG’s operating margins have tripled from a 3% base in FY16 to 9% in FY25, driven by gross profit growth, mix, and operating cost leverage. Rolex, while the largest revenue driver, carries a lower gross margin than other watches and jewelry – however, Rolex has much higher turnover, no discounting and requires minimal marketing spend, yielding exceptional returns on capital. As a result, we believe Rolex drives more than its share of profits, even at lower margins, thanks to volume and productivity.

A closer look at WOSG’s four-wall unit economics (chart below) shows that Rolex likely accounts for more than two-thirds of WOSG’s profits despite making up less than a third of the square footage in a typical store.

As such, Rolex sales are very accretive to profitability, generating returns on capital ~40%+ on our estimates. And continued price inflation for the top supply-constrained brands boosts gross profit per unit at no additional cost – effectively dropping straight to the bottom line.

Finally, regional mix is another margin driver, as U.S. stores, which command much higher average selling prices, should provide a natural lift to margins as the region matures and scales.

Source: Broyhill Asset Management Estimates; Brand Level ROIC = Adjusted EBIT / (Expansionary Capex + Inventory)

In the short term, our base case margin estimates are below consensus as we conservatively model additional downside from tariff uncertainty (management previously noted up to a 100 bps margin headwind, before the announcement of 39% tariffs on Switzerland). But we see margins expanding towards prior peaks by FY29 as mix shifts towards the U.S., where corporate infrastructure (distribution centers, regional HQ, etc.) remains underutilized relative to the potential store count. Investments have already been made and can support higher sales at minimal incremental cost.

While the tariff threat remains an overhang, we think the most likely outcome (as evidenced to date) is that increased costs are shared with brands and consumers via pricing, with limited retailer concessions as elasticity is extremely low at high price points, especially for waitlisted products, supporting pass‑through feasibility with minimal volume impact. Simply stated, tariffs may pressure reported gross margin percentages, but gross profit dollars are unlikely to change (a view consistent with brand announcements and negotiations to date). And unlike other retailers that see gross margins collapse with clearance, outside of the current tariff noise, gross margins have historically remained remarkably stable due to the industry structure – brands set margins which rarely compress because products aren’t discounted.

Bottom line: consensus EBITDA margin estimates around 11% in FY28-29, leave plenty of room for upside surprises given recent margins have hovered closer to 12%, and boom years north of 13%, which would put margins more in line with our bull case assumptions, given embedded operating leverage from continued scale across the U.S.

Capital Deployment

Unlike most retailers, whose only limitation on growth is the availability of capital to fund new builds, the pace of WOSG’s U.S. expansion is constrained by two factors – 1) Rolex’s desire and ultimate approval of new points of sale and 2) willing sellers of existing AD’s. As a result, the key debate around capital allocation is whether management can identify enough attractive targets to fuel their continued growth.

These investments have historically yielded attractive returns (we estimate >20% ROIC), as each acquisition brings greater earnings power, as well as the opportunity for store upgrades and greater allocations from brands. While consensus doesn’t explicitly forecast capital allocation moves, we see a lot of skepticism baked into sentiment. Our view is more optimistic. While management previously guided to a cumulative spend of £650-850 million through FY28 on acquisitions (£350-500 million) and new builds and renovations (£300-350 million) in their long-range plan, we have modeled a total of ~£500 million across our forecasts allowing for 5 to 16 in new builds and acquisitions, bringing the resulting FY28 store count to 213-224.

On our numbers, we see WOSG comfortably funding capital investments and M&A via internal cash generation, without endangering the balance sheet. The company ended FY25 with net debt of only ~£94M (excluding leases) or about 0.5× EBITDA, leaving plenty of flexibility. Should management decide to get more aggressive in their allocation of capital, a scenario we explore further in the Catalyst section that follows, we estimate the company has the capacity to fund continued expansion and a significant return of capital. For example, in our bull case we assume WOSG returns ~£200 million to shareholders cumulatively (representing >20% of the float) through FY2028 in accelerated repurchases, on top of our estimated ~£500m in investments, and leverage actually declines over that period.

Bottom line: we think the market is dramatically underestimating the incremental value creation from smart capital allocation. We see opportunistic buybacks at these prices as an excellent use of capital and a nice buffer for downside protection. Given management and the board are aligned on capital allocation, thoughtful capital allocation represents one of the most powerful upside drivers for shares.

What’s It Worth

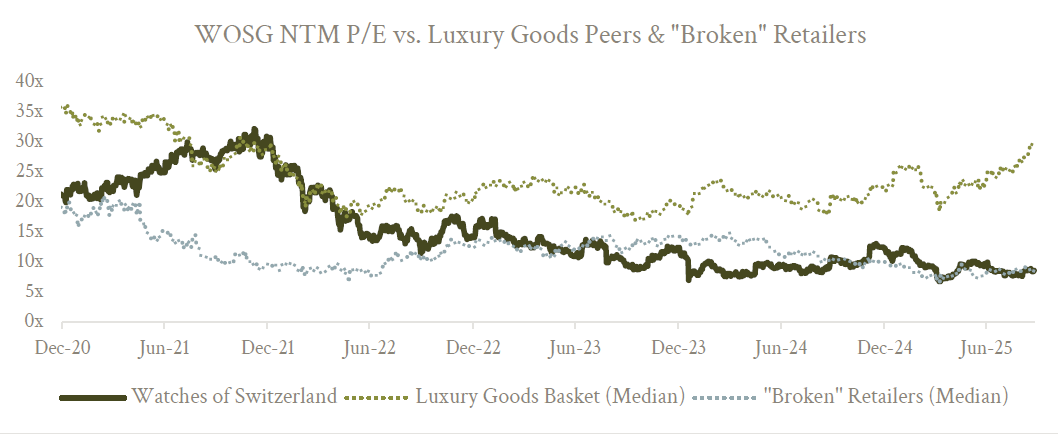

There are few perfect public comps for WOSG (most peers are either much smaller private dealers or large luxury brand owners). However, looking at related groups, we see European luxury brands trading at ~15–30× NTM EBITDA and U.S. specialty retailers trading as high as 15x NTM EBITDA. Meanwhile, even “broken” retailers with stagnant sales are valued as high as 7x NTM EBITDA, while WOSG currently changes hands for 5x depressed EBITDA (chart at the top of the following page), in line with Signet Jewelers, a mid-market, mass jeweler anchored to bridal cycles and mall traffic, with greater promotional risk and credit sensitivity.

Source: Bloomberg

As another point of reference, we analyzed historical transactions of luxury watch and jewelry retailers over the past decade to gauge a few different metrics. The median value of these transactions was ~ 1.0x EV/Sales and ~ 12.7x EV/Door. Notably, these valuations also reflect the often, under-optimized nature of mom-and-pop dealers, which WOSG then improves (through better inventory allocation, refurbishment, upselling, etc.) and effectively arbitraging that value. That caveat notwithstanding, these transactions imply valuations of WOSG from ~ £7 per share on an EV/Sales basis (with a ~£6-11 per share range) to ~£11 per share on an EV/Door basis (with a ~£3-24 per share range). The public market seems to be valuing WOSG as if it were just a sum of these parts, ignoring the platform premium and growth acceleration management has consistently achieved.

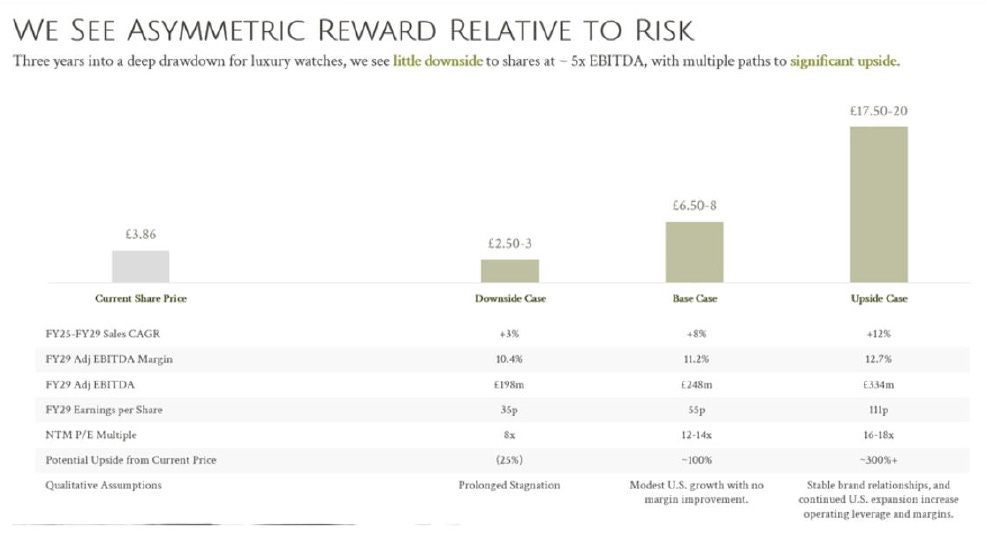

Putting it all together we see roughly 25% downside risk to shares with up to ~ 300%+ upside potential. In our bear case, assuming prolonged stagnation (low single-digit sales growth and continued margin compression, below overly punitive consensus expectations), we see a floor around 250–300p, implying 8x trough earnings). Said differently, a lot of bad news is already priced in. More realistically, our base case implies ~100% upside potential over three years, driven by high-single-digit sales growth, and modest EBITDA margin expansion to 11.2%, putting FY29 earnings at 55p. At 12x -14x earnings, we see fair value around £6.50 – 8.00 per share. Our bull case earnings estimates are roughly 2x higher at 111p driven by a more rapid US expansion and more aggressive share buybacks driving 12% sales growth and 12.7% FY29 EBITDA margins. At 16x – 18x earnings, roughly a 50% discount to the European luxury industry, WOSG could fetch £17.50 – 20.00 per share.

Bottom line: Given the stark disconnect between WOSG’s operational quality and its valuation, the market is offering investors an attractive asymmetric bet: limited downside (~25%) against potential returns of 100–300%, with the company trading below the sum of its acquired parts despite consistently demonstrating its ability to extract platform value. At 5× depressed EBITDA—pricing that implies permanent impairment rather than cyclical pressure—WOSG represents either a structural value trap or a significant mispricing. We think the evidence strongly suggests the latter.

Source: Broyhill Asset Management Estimates

Catalysts & Value Creation

The secondary watch market – the primary indicator for demand – has bottomed following a multi-year downturn, with WOSG poised to capture outsized growth as supply normalizes, consolidation reaccelerates, and Rolex CPO continues to ramp. We see a number of additional catalysts on the horizon providing ample runway for shares to grind and re-rate higher.

Clarity on Rolex–Bucherer Dynamics. Any clarification from Rolex that Bucherer’s acquisition hasn’t changed anything (so far, all evidence points to no change) would remove a major overhang. For example, Rolex could renew long-term supply agreements or grant WOSG new mono-brand boutiques (if WOSG announces, say, new Rolex stores in Chicago, that would be a catalyst confirming Rolex’s support). The most important signal here would be accelerating growth in net new doors in the US (via acquisition or continued new openings) along with increased allocations, refurbishments, or relocations. As it becomes clear that Bucherer’s integration into Rolex’s orbit caused no harm, and WOSG keeps reporting solid results with no change to allocations, this overhang should gradually fade driving a substantial re-rating towards a more normal, premium valuation as fears subside.

Clarity on Tariffs, Consensus Reset and Credibility Rebuild. Any suspension or rollback of tariffs would ease fears and likely spark an immediate rally in WOSG and across the luxury sector. Yet at the current valuation, clarity in itself would suffice to clear the decks. It would also provide management with the visibility to update its now stale Long Range Plan and host a much-anticipated Investor Day. We think a refreshed long-term guide would serve as a clearing event for shares, as the bar has been sufficiently lowered after years of downgrades and negative earnings revisions. If updated numbers are credible and the company executes, renewed growth in the U.S. should drive upward revisions to earnings and multiple expansion, closing the gap to luxury peers.

Continued U.S. Expansion. Retail valuations are closely correlated with new store growth and WOSG is no exception. While the stock’s valuation has derated alongside slowing store growth, as Rolex and other top brands reduced allocations to manage COVID-era supply imbalances, we have good visibility into management’s plans through 2027 which include new openings in Southdale Center, MN, University Town Center, FL, and Avalon, FL, in addition to a significant pipeline of flagship refurbishments that have historically been followed by increased allocations. At the same time, a sizable acquisition of a larger chain would be a major catalyst, although the timing of any transaction is impossible to predict. Still, with plenty of under penetrated markets, and independent jewelers facing succession issues, acquisition targets at attractive multiples remain well within WOSG’s balance sheet capacity. We see WOSG’s ongoing expansion of their US footprint as the highest and best use of capital, in addition to the most logical path to a rerating. If management (or Rolex) indicates increased production or allocations, we believe that news would immediately boost sentiment - Rolex’s December 2023 announced plan to build a major new facility in Bulle, Switzerland reinforces the long-term supply growth story.

CPO Expansion & Secondary Market Stabilization. Rolex CPO is ramping aggressively, and already represents WOSG’s second largest brand behind Rolex, at 5-10% of sales in just a few years since launch. Increasing residual values (CPO generally sells at 25% - 30% premium to the secondary market) improves conversion on core brands, supports trade-in activity, and drives further CPO volumes. In May 2025, Rolex widened certified pre-owned eligibility from 3+ years to 2+ years old, increasing inventory throughput and price points, improving velocity, gross profit dollars, and customer acquisition. We also see a significant tailwind for CPO sales as the quality of counterfeits flooding the market are increasingly difficult to distinguish from the genuine product. Continued execution here means faster turns and richer attachment on services, jewelry, etc.

VAT Free Shopping in the UK. The reinstatement of tourist VAT-free shopping in the UK – there’s ongoing lobbying to bring it back – would provide a material boost to sales in the region, which have been under-earning due to the tourist void, and an immediate catalyst for shares. While we don’t assign a particularly high probability to this outcome, the impact would be significant and immediate, likely adding several points to UK sales growth.

Importantly, we don’t think we need any of these for the stock to work over time (at this price, earnings growth alone should provide attractive returns to the equity), but we do think any combination of the catalysts here would drive a rerating in the multiple back towards luxury peers. That said, we do have a few suggestions to drive change should the stock continue to languish in the medium term.

While we regard current management among the best in the industry and have no interest in influencing the company’s day-to-day operations, we do see meaningful opportunities to accelerate value creation for all shareholders.

We think there are two areas in particular - sharper capital allocation and capital structure optimization - where our experience and shareholder perspective can be especially additive.

First and foremost, we believe the company’s balance sheet is extremely underleveraged and given the tremendous disconnect between our estimates of intrinsic value and the current stock price, we see a more aggressive share buyback as a direct path to unlocking that value. While U.S. companies are generally open to stock repurchases, we have found European boards and management teams to be much more conservative in this regard, particularly when repurchases are funded by debt. Considering that WOSG was over 5x leveraged before coming to market in 2019 (and likely carried more debt in the hands of private equity before the IPO), we believe the business model can and should run with more leverage than the current half a turn on the balance sheet (excluding operating leases). We modeled scenarios illustrating that even one or two turns of leverage would enable the company to repurchase 10% - 20% of the float, while leaving ample liquidity to fund capital investments and pursue value accretive acquisitions as they become available.